Our sponsor’s at Kelly + Partners have shared their exclusive conversation surrounding Strata Schemes and Tax Time.

Joel Russell (JR): Peter, you’ve worked with Strata managers on complex tax matters for some time now. What are some key considerations for a strata manager when approached by an owner about tax?

Peter Cohilj (PC): Joel, I think the key thing we must consider is risk mitigation.

JR: For example?

PC: I’ve been called on to provide Key Witness Reports in various court cases where even verbal representations, tax matters discussed over the phone have been taken as Tax Advice. A strata manager needs to tread extremely carefully and certainly not provide income tax advice unless they are a registered tax agent or solicitor.

JR: But tax is straight forward isn’t it?

PC: Clearly, you are being facetious. It is, until it isn’t. It’s complex legislation and often spits out unexpected results. And further, such matters are unlikely to be covered by your professional indemnity insurance.

JR: But in the “real world” Peter strata managers are getting asked tax related questions by owners all the time. How do ensure that something isn’t construed as tax advice?

PC: Again, Strata managers need to tread carefully, matters relating to income tax are beyond the scope of the services they are providing. Obviously, they have had some exposure to these issues, so I would recommend something like…”in my experience I have seen it handled this way, however I’m not in a position to provide you with Tax advice. I recommend that you seek professional Taxation Advice”

JR: Or words to that effect.

[PC nods] Got it.

JR: So, what are some of the strata related tax matters coming across your desk at the moment?

PC: Truly tax effective scenarios require a Tax specialist and a lawyer well versed in Strata Law working hand in hand. Understanding the interplay of Taxation law and Property law is fundamental to tax effective outcomes. Many transactions I’ve been involved with can give rise to significant income tax, GST, capital gains tax and stamp duty implications for the both the lot owners and the owners corporation. Changes in ownership of common property; the creation of exclusive use rights over common property, for example car parks; compulsory acquisition of common property by the government; Embedded Networks…

JR: Sales or lease of roof space for Telcos…

PC: Yes Definitely, and interestingly the Sale or Lease scenarios each have different tax consequences.

JR: Seek advice before the transaction has occurred?

PC: Of course, not after the horse has already bolted. Retrospective tax advice is…useless.

Peter, still on the Telco Tower example. Tax on Non-mutual income from Common property is currently taxed in the hands of the individual lot owner. Do the lot owners have to receive this in cash for it to become taxable in their hands?

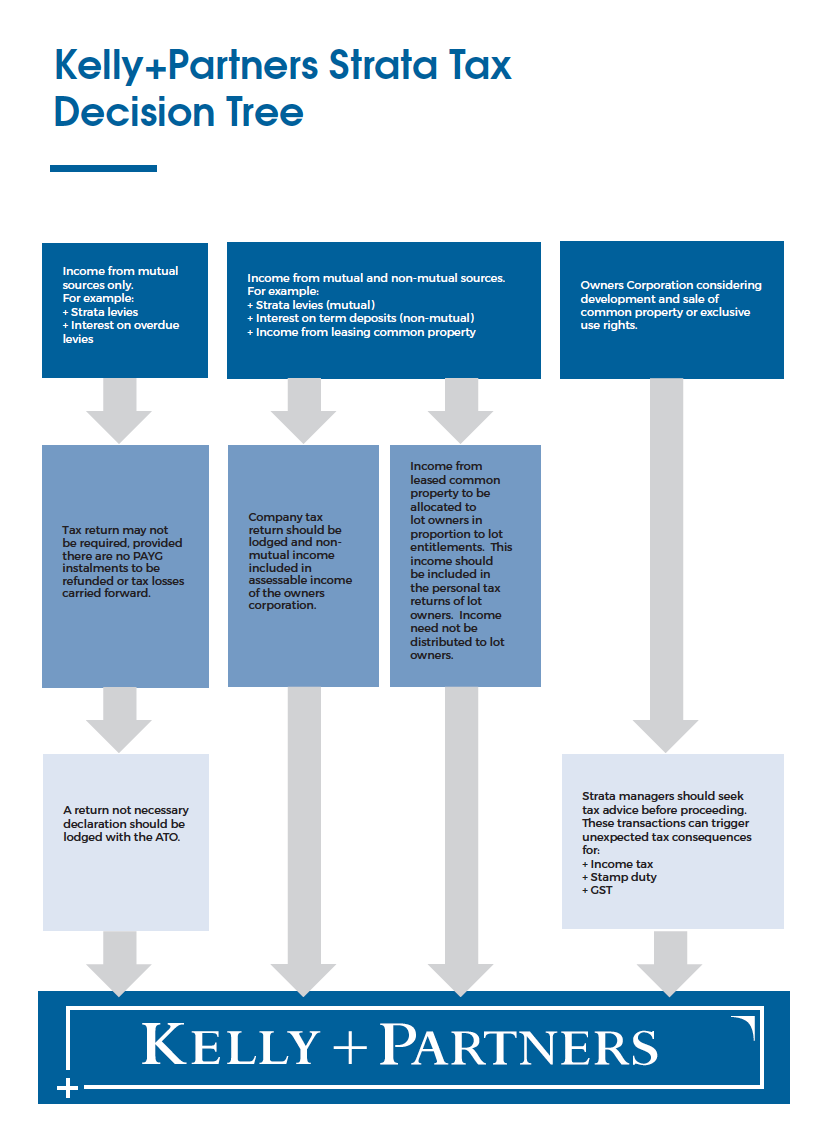

PC: No, where the income is retained within the plan the lot owner receives the economic benefit via reduced levies. It remains taxable in their hands. Currently, the Commissioner treats any income generated from common property as assessable income to the lot owners and not the body corporate. Any rental income or capital gain is assessable to the lot owners based on their unit entitlements. Similarly, any deductions relating to the common property can be claimed by lot owners depending on their unit entitlements.

JR: I hear of many owners complain to their strata managers over the need for their body corporate to lodge tax returns where taxable income is nil. But tax law distinguishes between “assessable income” and “taxable income”, which one triggers a tax return?

PC: Bodies Corporate are required to lodge an income tax return for any income year in which it has earned $1 in “assessable income”. For example, bank interest, search fees, dividends. A tax return is required irrespective of whether the body corporate has a net taxable income after allowable deductions. And in answer to the owner who asks “why?”. It’s the law unfortunately.

JR: Over recent years we have observed some strata managers and even tax agents applying the 28.5% tax rate applicable to small business. In your view, is a body corporate eligible to be taxed at this concessional rate?

PC: Bodies Corporate are taxed as companies. The reduced corporate tax rate of 28.5% rate applies to companies that are a “small business entity”. The general activities undertaken by a body corporate generally does not constitute the carrying on of a business and for this reason the body corporate should be subject to a tax rate of 30%. This has been clarified.

JR: The SCA in several states has been notified that there are businesses and individuals within this industry preparing and lodging tax and BAS who are not registered agents. Would it be within the realms of possibility that the TPB may turn its eye towards unregistered practitioners across the strata industry?

PC: Possible and with their additional $20mill funding probable. Under the tax agent services act anyone who prepares or lodges an income tax return and/or a BAS for another person and charges a fee must be a registered Tax Agent or BAS agent.

JR: But what if they don’t charge for it, acting as a “Public officer” across their entire portfolio per se?

PC: Still gone. If the person charges for other services and does not charge separately for tax or BAS services, it is still illegal. This is called “bundling”. An example of bundling is where a management fee includes tax or BAS preparation and lodgement. If the tax service is an “inclusive” item on the management contract. Gone. Penalties of $42,500 for an individual and $212,500 for a corporation.

JR: Ouch. For each instance?

PC: Yes.

JR: From an investor’s perspective. where do investors currently stand in relation to the deductibility of strata levies? Are special levies 100% deductible where they relate specifically to an identified capital expense?

PC: Investors can generally claim an immediate deduction for quarterly strata levies. However, a special levy raised for capital improvement and capital repairs, is not immediately deductible.

JR: So, assigning a Special levy to a specific capital expenditure item rather than funding it from a fully funded Sinking Fund can have a different tax outcome?

PC: Potentially. Ultimately, it’s a timing thing. While special levies may not be immediately tax deduction, lot owners who are earning rental income may be eligible for depreciation on the building and other fixtures. This can include building works acquired through special levies.

JR: Are we talking just the original owners here?

PC: Subject to conditions being satisfied, owners need not have been an original owner of the lot to claim depreciation. A building depreciation report must be obtained from a suitably qualified professional.

JR: So, the final word on a strata manager fulfilling their fiduciary obligations in relation to tax related matters?

PC: If I could re-emphasise just one point it’s that when communicating with body corporate and lot owners it is imperative to make it clear that you have not provided any tax advice. As the tax implications can be significant, you should always advise the body corporate and the lot owners to obtain tax advice so that they are appropriately informed. It is imperative that advice be sought prior to entering into any agreements or arrangements.

JR: Is ignorance a legally defensible position?

PC: Joel, I welcome you to put it to the test, but I sincerely doubt it.

JR: Ouch. Peter Cohilj as usual, it’s been a pleasure.

PC: You’re most welcome.

Kelly + Partners have also provided a simple flow chart outlining the decision making process for Bodies Corporate relating to tax matters.

{kind=link}